A Guide to Your 2021 Tax Season in Canada

Spring has sprung, and that means warm weather, backyard barbecues and more are on the horizon! But, every spring, every Canadian adult in charge of their own finances has to make it over a major hurdle before they get to enjoy the sunshine - that is, the annual practice of filing one’s taxes.

This is primed to be an interesting tax year thanks to COVID-19, so if you haven’t started organizing your tax materials yet, it’s definitely time to get started. Despite the ups and downs of 2020, the Canada Revenue Agency didn’t extend the deadline to file this year as some thought they might. Most Canadians must file their taxes by April 30, 2021, though if you’re self-employed, you have until June 15. One of the major changes this year is that the CRA is actively requesting people file online if at all possible. This is another effect of the pandemic - the CRA has reduced capacity this year to receive and assess paper filings, so they’re estimating that a paper return might take around 10-12 weeks to get a proper assessment.

To begin our discussion about the 2021 tax season, we’ll ease you in with our favourite part. Though it varies every year, many Canadians look forward to late spring when they receive their tax return. It’s so tempting to earmark that money for consumption, and that’s ultimately what the government wants you to do too. Assuming you spend yours at a Canadian business, that money gets pumped back into the economy and helps to fuel growth (naturally, a high priority for the country after 2020).

However, we challenge you to do something different with your return this year - save it! This isn’t to say that it’s not important to treat yourself sometimes. Conversely, building rewards into your financial plan is likely to help you stay on track with your goals more so than trying to go without any enjoyment as you save. But, saving your return in a place where it’s going to earn a high interest rate is going to pay off in a big way that spending it just can’t beat.

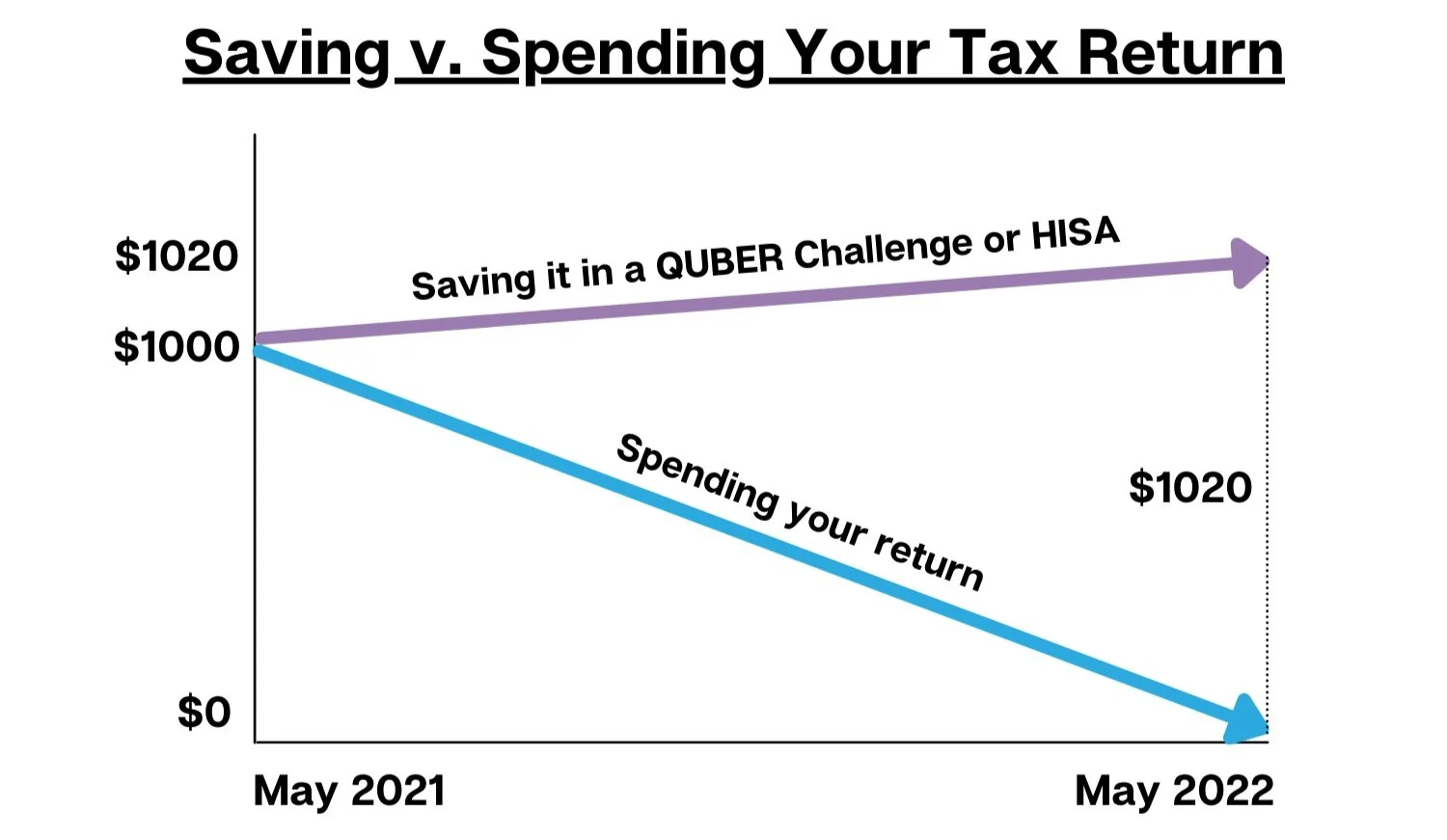

Let’s say you get $1000 as a return this year. You see two possible options for that money: you could spend it on new clothes you’ve been dying to get for months, or you could save it. For the purpose of our example, let’s assume you’re considering saving it through a QUBER $1K Saving Challenge where you’ll earn a 2% incentive when you finish the Challenge, but you could save it in any high-interest savings account. Spending it on clothes is probably going to be fun, and you do legitimately need clothing - it’s an essential expense and an unavoidable part of life. But, that’s all your tax return will ever be: you’re left with $0. Clothing depreciates in value from the moment you buy it, meaning you’ll never be able to sell it for as much as you bought it for. You may also decide in a few months that you don’t love your new pieces as much as you did when you bought them, or you may be forced to stop using some due to damage or wear.

Instead, if you save that $1000 over the course of the year into your $1K Saving Challenge, you’ll still have that $1000 come spring 2022 AND you’ll have earned a $20 incentive for finishing the Challenge. Plus, unfortunately, sweaters cannot be used as currency to pay bills or rent. You may face a financial emergency at some point this year, and having an extra $1000 might make all the difference in how you’re able to bounce back. Ultimately, would you rather have $0 or $1020 in a year’s time? Spending your tax return is enticing, but the temptation to buy things never really goes away for most people; spending your return isn’t likely to quell that fire. Saving it instead offers you the chance to earn interest, pad your savings and give yourself peace of mind when it comes to potentially facing a sudden financial shock over the coming year.

P.S: QUBER offers users a free, easy to use and fun digital savings account where they can earn cash rewards just for saving money. If you want to join thousands of other Canadians and get set up so you’re ready to save when you receive your return, click here.

With returns covered, we’ve also got to tackle a bit of the less-exciting stuff. The biggest point of concern for many Canadians this year is the degree of impact that the emergency benefits they collected in 2020 will have on their tax responsibilities. There were a number of types of benefits offered by the Canadian government when the pandemic first hit, including CERB (Canada Emergency Response Benefit), CESB (Canada Emergency Student Benefit) and CRB (Canada Recovery Benefit) among others.

Due to the immediate nature of many Canadians’ needs, most emergency benefits were not taxed at the time they were paid out (some types, like the CRB, were taxed 10% when they were issued). However, all the benefits given out in 2020 are considered to be taxable income. So, the amount of income you actually earned from employment plus the amount you received in emergency benefits is the amount that’ll determine your tax rate for when you file this year. For example, if you collected $18,000 in employment income + $6,000 in CERB payments in 2020, your marginal tax rate will be based on $24,000 as your total income for the year.

For some, this may increase their tax responsibilities in a considerable way, as they might be pushed into a higher tax bracket than they’d have been in otherwise. Though we just went on about saving your return, if you collected benefits, you may find for the first time in your life that you actually owe taxes. If you did collect emergency benefits, the government should have sent you a T4A or a T4E tax slip in February that includes the total amount of benefits you received. You’ll need this information to file accurately, so if you haven’t received yours yet, you’ll need to contact the CRA or check your My Account online.

The government does acknowledge that given the tumultuous nature of 2020, paying back the taxes they owe may be very challenging for a number of Canadians. Not everyone has recouped the loss of income they experienced due to the pandemic, and asking them to fork over a chunk of their savings to foot a tax bill before April 30 would be crippling. As such, if you have an annual income lower than $75,000 or you collected emergency benefits this year and you owe taxes, you have until April 30, 2022 to pay your 2020 taxes before being charged any interest. Any Canadian who doesn’t fall into this category is still required to file and pay their taxes by April 30, 2021 as usual. Note that even if you now have until 2022 to pay, you still need to file before April 30 this year - if you don’t, you’ll be charged a late-filing fee.

Beyond just paying taxes on CERB and other emergency benefits, there are a number of cases where those who received benefits must repay them to the government. Due to the immediate need Canadians faced for liquid cash last spring, the government made it easy for people to access benefits quickly without jumping through too many hoops. However, now that tax season has arrived, those who received benefits they shouldn’t have are on the hook to repay what they owe. This may apply if you accidentally received more payments then you should have or you collected benefits you were actually ineligible for. If you’re unsure if you have to repay what you received, note that the government will have contacted you to clearly state that you owe them.

However, again, the government knows that asking for repayment from people who had a difficult financial year in 2020 is a tough ask. In contrast to the way a private creditor might hound you down to repay your debts, the government isn’t going to enforce penalties or charge you interest on emergency benefits repayments. The CRA’s website even says that they’re willing to create flexible repayment plans on a case-by-case basis if you contact them to arrange it, so if you know you’re going to be stuck with a bill to pay, this may be your best bet!

Another important thing to remember come tax-time is to be vigilant in protecting your personal and financial information. Knowing that a call or message from the CRA this time of year might need your immediate attention, fraudsters across the country know it’s an advantageous time to pretend to be someone from the CRA who needs sensitive information. Think critically about how the CRA would or would not contact you, and if something seems fishy, it probably is! If you can and haven’t already, set up a My Account profile with the CRA. It’ll give you all your important tax information in one place, allow you to file online easily and you’ll know you have a secure line of communication with the CRA through it.

Before we leave you, there are some new tax credits available this year which may help to reduce your overall liability if you’re eligible to claim them. For those that work from home, the government has introduced a home office tax credit that allows those who were forced to take up remote work to claim a credit for paying for expenses like internet, water and heat that would usually be covered by your employer during the work week. To make calculations straightforward, the CRA says eligible Canadians can claim $2 for every day they worked from home last year up to a maximum of $400 (so, up to a maximum of 200 days). Note that this only applies to work days - you can’t claim weekends if you don’t work on Saturday and Sunday!

If you don’t work from home but did pay for some kind of tuition or training in 2020, you may be eligible to claim the newly introduced Canada Training Credit. At the end of 2019, eligible Canadian workers between the ages of 25-65 started accumulating an annual sum of $250 in what’s known as the Canada Training Credit account. The account has a lifetime maximum of $5000. Starting this year, those who paid for schooling can claim either the full balance of their account or up to half of their tuition/training expenses (whichever amount is lower), and everything that doesn’t get used can be claimed in future years. To confirm if you qualify for the program, you’ll need to check with the CRA.

If neither of the above apply to you but you are a news junkie, there’s an interesting new credit that allows Canadians to claim up to $500 back if they purchased news from a pre-approved Canadian digital media outlet in 2020. To be included on the list, the news outlet must be without a broadcast license (meaning they aren’t licensed to broadcast on the radio in their specific area of the country) and they must be providing mostly original news content to their subscribers. It includes both digital service and home delivery for Canada’s biggest newspaper, The Globe and Mail, so definitely worth looking into if you’re a subscriber! You can find the full list of approved outlets here.

Final Thoughts

As you’ve likely heard before, the only things that are guaranteed in life are death and taxes. The sooner you start preparing your tax return, the more time you have to check your work or have it checked by a professional to ensure you’re on the right track. If you’re not feeling confident about compiling your return on your own, remember that putting it off doesn’t serve you in the slightest! Invest in some tax software to help check your work and highlight all the credits you could be claiming this year. Plus, as most Canadians earn less than $75,000 a year, even if you owe taxes this year, you know you’ve got some flexibility in regards to getting them paid back over the next year. Like many things with personal finance, tax season isn’t considered to be “fun” by most, but it definitely need not be scary if you tackle it head-on. You’ve got this!

Check back to Money Talks every Monday for a new post featuring more tips on how to reach your saving goals, and subscribe to our mailing list for blog updates! Have a suggestion for something you’d like us to write about? Shoot us a message at contactus@quber.ca and we’ll get to work.