TFSA’s: Everything You Need To Know

We’ve made a point to ask our users what they want to accomplish with their money in 2021, as we want to know how we can best support our user base’s efforts to manage their finances this year. It seems that many of you have been thinking about how to make your money work for you effectively, and one of our most popular requests was to learn more about TFSA’s. A Tax-Free Savings Account, often referred to as a TFSA, is a registered savings account that allows people to grow their wealth without paying taxes on it. Whereas a standard bank account is non-registered, a registered account is approved by the government to hold a sheltered tax status. That means, each tax season, the amount held in your registered accounts (including any income you may have earned from investments held in them) will not be considered when calculating what taxes owe. Even when you withdraw income from a TFSA, you won’t be taxed on it, as any deposits you make in a TFSA to begin with are after-tax (you already paid income tax on it once when you earned it).

TFSA’s are actually rather straightforward, and the impact they’ll have on your tax responsibilities are easy to grasp; the idea of having one need not intimidate anyone. In that light, we wanted to compile some of the key points on TFSA’s that all adult Canadians should be familiar with. If you already have a TFSA, it may help you reassess your contribution strategy. If you’ve never had one before, it may help to highlight the major opportunity for tax reductions that you’re missing out on by not having one.

Here are the basics you need to know about TFSA’s in Canada:

Anyone over the age of 18 with a valid SIN (social insurance number) is eligible to open a TFSA. You do not need to be earning a certain amount of income to have a TFSA, and you do not need to meet the contribution limit each year to keep one active. You can open a TFSA with most financial institutions, including banks, credit unions, insurance companies and trust companies. Though you won’t be taxed on the income you save and earn in a TFSA, you still may be liable for any fees related to the maintenance of the account from the issuing financial institution.

The main thing you’ll need to keep in mind when it comes to TFSA’s is your contribution limit. This is the central point you’ll need to work around as you manage your TFSA year-to-year. The amount which any individual may contribute to their TFSA in a given year is known as the contribution limit. This is the only “downside” to having a TFSA (it’s not really much of a drawback, but will limit the size of your tax shelter). The limit changes each year, but is a set number; everyone who holds a TFSA in Canada is awarded the same annual contribution limit.

The maximum amount any Canadian may have in their TFSA in 2021 is $75,500. Though you can hold any amount of money in a TFSA up to $75,500, that is the defined legal maximum limit any Canadian may hold in their TFSA today. This number is the sum of the contribution limits from each year since 2009, the year the TFSA program was introduced in Canada.

The contribution limit for 2021 is $6,000. However, your true contribution limit for the year is likely going to be different. Your contribution limit may be higher than $6,000 if you’ve made withdrawals from your TFSA in previous calendar years and have yet to replace those funds, or if you’ve not met the accumulated contribution limit of $75,500.

The annual contribution limits for each year since 2009, the year the TFSA was introduced in Canada, are as follows:

2009 - 2012: $5000 each year

2013 - 2014: $5500 each year

2015: $10,000

2016 - 2018: $5,500

2019 - 2021: $6,000 each year

= $75,500 (total maximum amount in any Canadian TFSA)

Every Canadian TFSA holder is entitled to save up to the maximum of $75,500. If you haven’t saved much in your TFSA or you’re just opening one now, you have the opportunity to save much more than just the standard contribution limit for this year. This is so that people who start saving into a TFSA today aren’t disadvantaged by factors like their age, or their income level. Otherwise, those who were eligible to start saving into a TFSA in 2009 when they were introduced would forever have a permanent advantage over all those who opened their TFSA’s later than 2009; people who start today would only be able to save a fraction of those who came before them. Even if you didn’t file income taxes in certain years since 2009, you’re still entitled to the same accumulated contribution limit as everyone else in Canada.

So, if you’re just opening your first TFSA in 2021, your annual contribution limit for this year is $75,500. This gives you the opportunity to save as much as those who started in 2009 have, if you can afford to do so. If you have a TFSA but haven’t met the contribution limit in any year leading up to 2021, you are eligible to save this year’s limit plus the total amount that you didn’t save in previous years. For example, if you opened a TFSA in 2018 and met your limit in 2018 and 2019, but then only saved $2,500 in 2020, your limit for 2021 will be $9,500. This is because you’ll be able to save the annual limit of $6000 for 2021, and an additional $3,500 due to the fact that you only saved $2,500 of your $6,000 limit in 2020.

If you withdraw money from your TFSA, that dollar amount is added to your contribution limit to the next calendar year. If you need to withdraw money from your TFSA, you can do so without fear that you’ll lose the ability to contribute that amount again in the future. So, for example, if you withdraw $3000 from your TFSA in October 2020, your contribution limit for 2021 will be $9000 ($6000 annual limit + $3000 withdrawn in 2020 = $9000 total for 2021).

You can withdraw from most TFSA’s at any time. However, if you withdraw from your TFSA, you can only replace funds up to your contribution limit for that year. For example, if you deposit $5000 in February this year and then withdraw $4000 in August 2021, you can still only deposit an additional $1000 in your TFSA before the end of 2021 to make up $6000. That $4000 you withdrew won’t be added to your contribution limit until 2022.

From the above principles, to calculate your contribution limit, consider the annual limit, plus any withdrawals you made in previous years plus any unused contribution room from years since 2009. The lowest your contribution limit can be in 2021 is $6000, because everyone is awarded $6000. Most people, however, will have a much higher limit this year due to past withdrawals and unused contribution room.

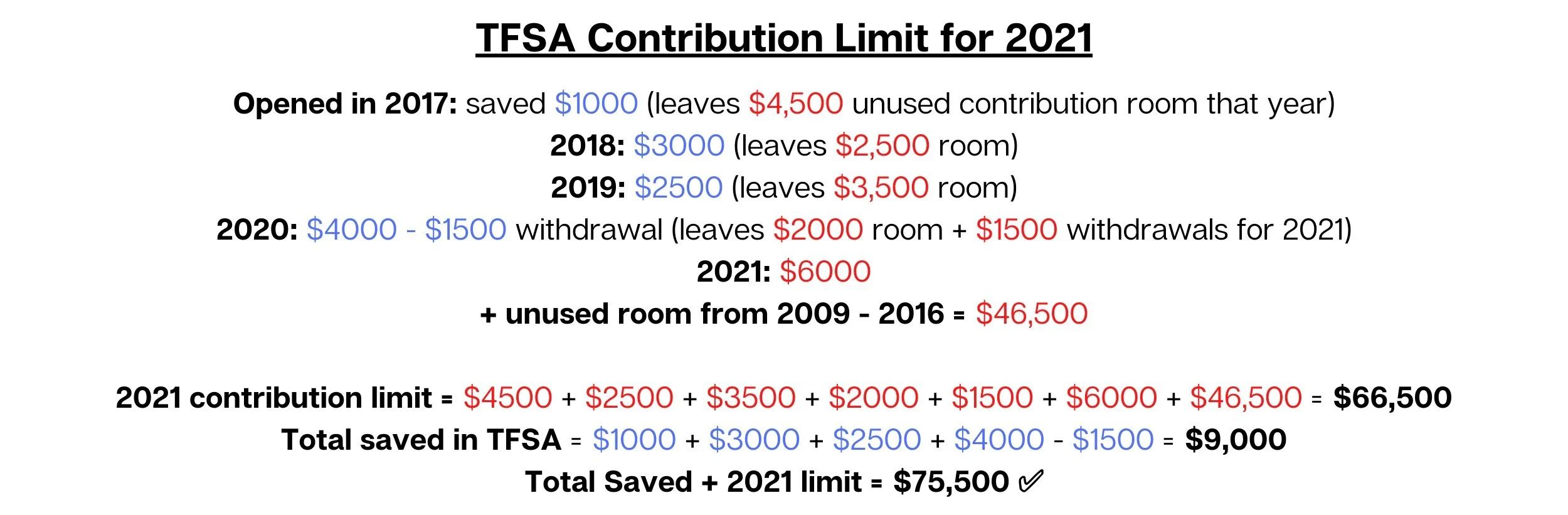

For example, let’s say you opened a TFSA in 2017. You saved $1000 that year, then $3000 in 2018, $2500 in 2019 and $4000 in 2020. You also withdrew $1500 from your account close to the end of 2020. You would calculate your contribution limit for 2021 as follows:

Use the maximum of $75,500 as a check to determine if you’re on the right path. If you add up your contribution limit and the total amount that you’ve saved in your TFSA/s today (note: this doesn’t include any income earned or lost on investments in your TFSA), it should equal this figure. If you’re coming up with another number, that’s a sign that you need to go back and check your work.

You may store a variety of investments into a TFSA. This includes cash, mutual funds, securities listed on a designated stock exchange, guaranteed investment certificates, bonds and certain shares of small business corporations. You may also deposit foreign currency into a TFSA, but only if its equivalent amount in Canadian dollars (CAD) falls below your annual limit.

You can have more than one TFSA, but the contribution amount across them must not equal more than your total contribution limit for the year. You can split your TFSA contributions amongst numerous different registered accounts, but you cannot save more than your total contribution limit for that calendar year.

Any income you earn through your TFSA (such as income earned on investments) will also be excluded from taxes, and will not affect your contribution limit. That means, if you’ve got investments held in your TFSA that are performing well, there’s no need to worry about it affecting your ability to contribute to your TFSA that year. So, for example, even if you have an investment that earns $5000 in your TFSA in 2020, you still get to contribute $6000 in 2021.

This is one of the key factors to remember as you manage your TFSA and other investments. If you’ve got high-performing investments and you can put them in your TFSA, you should. That’s where it’ll be awarded the highest level of tax advantage, and you’ll be able to keep everything you earn from those investments without paying taxes on your gains.

In a similar manner, any losses you incur on investments held in a TFSA will not affect your contribution limit. Though investments you hold in your TFSA might lose money while they’re held in it, that is not the same as withdrawing money from your TFSA. As such, investment losses won’t give you an advantage on your contribution limit for the next year. For example, if you have an investment in your TFSA that loses $3000 in value over the course of 2020, that does not raise your contribution limit by $3000 for 2021; you will still face the same $6000 annual limit as everyone else.

There is no “magic stop” when it comes to TFSA contributions. By that, we mean that neither your TFSA nor your financial institution will stop you from over-contributing to your TFSA. Your account can hold more than your legal contribution limit, meaning you need to be mindful of your your transfers to and from your TFSA for the year. If you are found to be holding more in your TFSA/s than you’re legally permitted to, you’ll get taxed on that excess amount at a rate of 1% until you remove it from your account.

The CRA obtains TFSA information each year by collecting it from issuers by the end of February each year. That means, if you have a TFSA, you cannot stop the Canada Revenue Agency from collecting tax information in regards to that account. Information is collected through the issuer of the TFSA, not the account holder. By opening the account with whichever financial institution you pick, you are agreeing to register that account with the government for such purposes.

If you hold a TFSA, you are legally the only person who has control over it. As a TFSA account holder, you are the only person who can make contributions to your TFSA, withdraw from it or determine how to handle investments within it. You may appoint a representative on your behalf, such as a spouse, who may collect and provide tax information for you though.

The annual contribution limit for 2021 split into even payments over one year equals out to roughly $115.40 weekly, or to just over $230.75 bi-weekly ($6000/52, and $6000/26, respectively). If you’re looking to meet the contribution limit this year, this is how much you’d need to save into your TFSA on a weekly or bi-weekly basis over the course of 2021.

Saving into a TFSA is different than saving into another type of popular registered account, the RRSP (registered retirement saving plan). Though there are many similarities between the two types of accounts, there are a number of key differences to consider. They are summarized as follows:

The money you save in a TFSA is tax-exempt from the time you deposit it, even when you withdraw it. When you withdraw money from an RRSP, you will be taxed on that money.

In the vast majority of cases, there are no penalties or fees for withdrawing from your TFSA like there is with an RRSP. The only penalties associated with TFSA’s are handed out when people over-contribute, as mentioned above.

An RRSP contribution is made with pre-tax income, which is what allows you to defer paying taxes on it until you withdraw it. A TFSA contribution is made with income that’s already been taxed.

Saving into a TFSA on its own is helpful, but it has a more powerful effect when it’s used in combination with other registered accounts. A TFSA is an excellent tool to employ if you’re trying to grow your RRSP. As you’ll be taxed on any money you withdraw from your RRSP (it must be reported as income in the year you withdraw it), it’s in your best interest to be withdrawing that money only when you’re truly retired. Otherwise, you’ll pay taxes on that money at your current tax bracket as an employed adult, instead of at the very low tax bracket you’ll enter when you retire. Instead, if you can save into a TFSA and an RRSP simultaneously, you’ll have the freedom to take from your TFSA as you need to without worrying about incurring any penalties or about the effect it’ll have on your taxes that year. That way, you can leave your RRSP alone until you’re actually retired. In this way, your TFSA can act as a financial bridge between today and your retirement, and will help to minimize the amount you’ll pay in taxes on what you’ve put away for when you don’t have a steady source of income anymore.

We hope these tips help you navigate the world of TFSA’s, and encourage you to open one if you’ve never done so before. Though you may pay a small amount in bank fees to maintain your TFSA, the benefits of having one and regularly saving into it far outweigh that cost. If you’re ready to take the next step with your money, you need to be thinking about ALL the different ways you can reduce your expenses over the course of your life, and minimizing your lifetime tax bill is an excellent place to start.

Check back to Money Talks every Monday for a new post featuring more tips and tricks on how to reach your saving goals, and subscribe to our mailing list for blog updates!

Have a suggestion for something you’d like us to write about? Shoot us a message at contactus@quber.ca and we’ll get to work.